blog

Insurance, a risk worth taking?

Blog — 10 Nov 2021

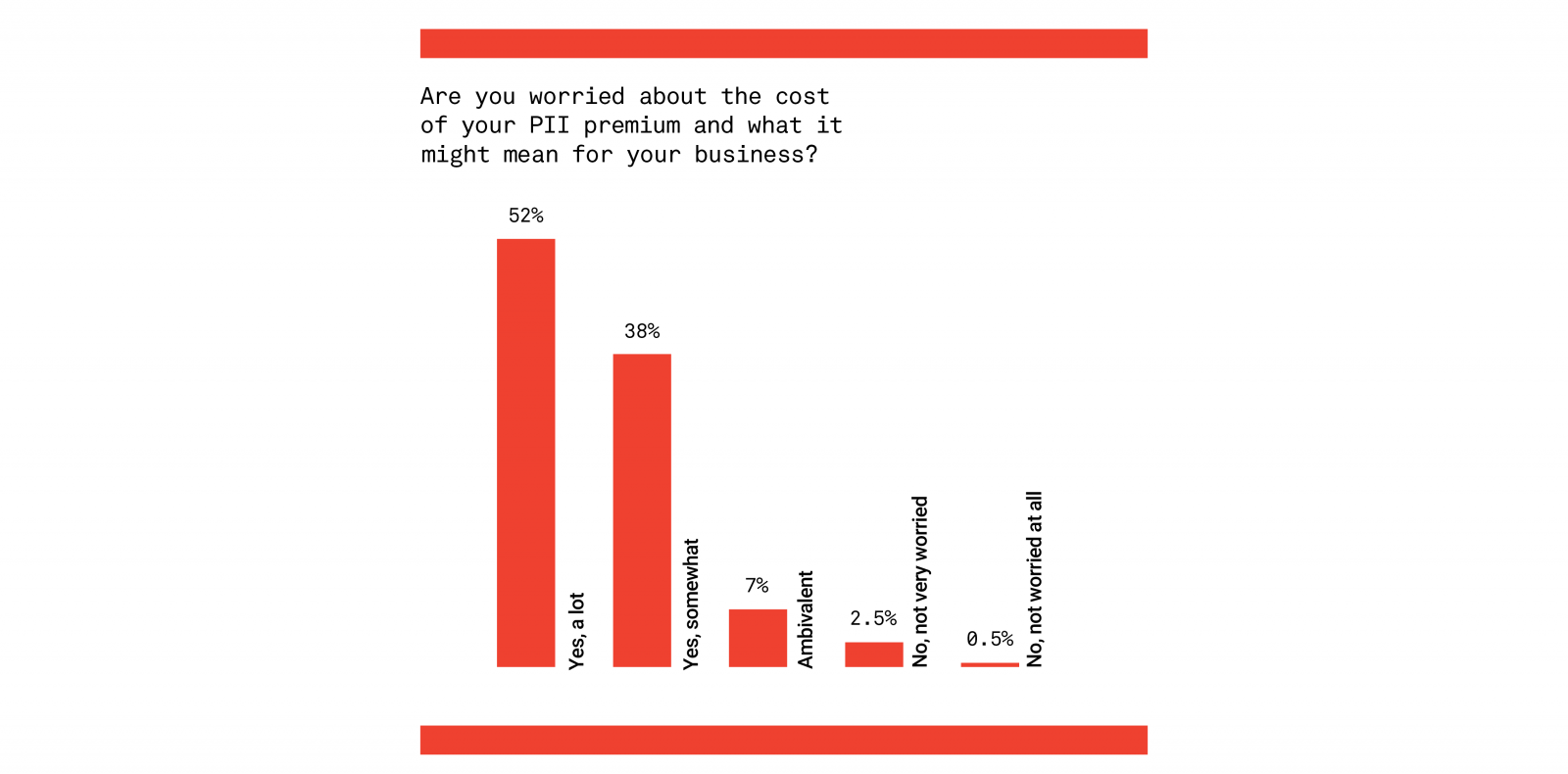

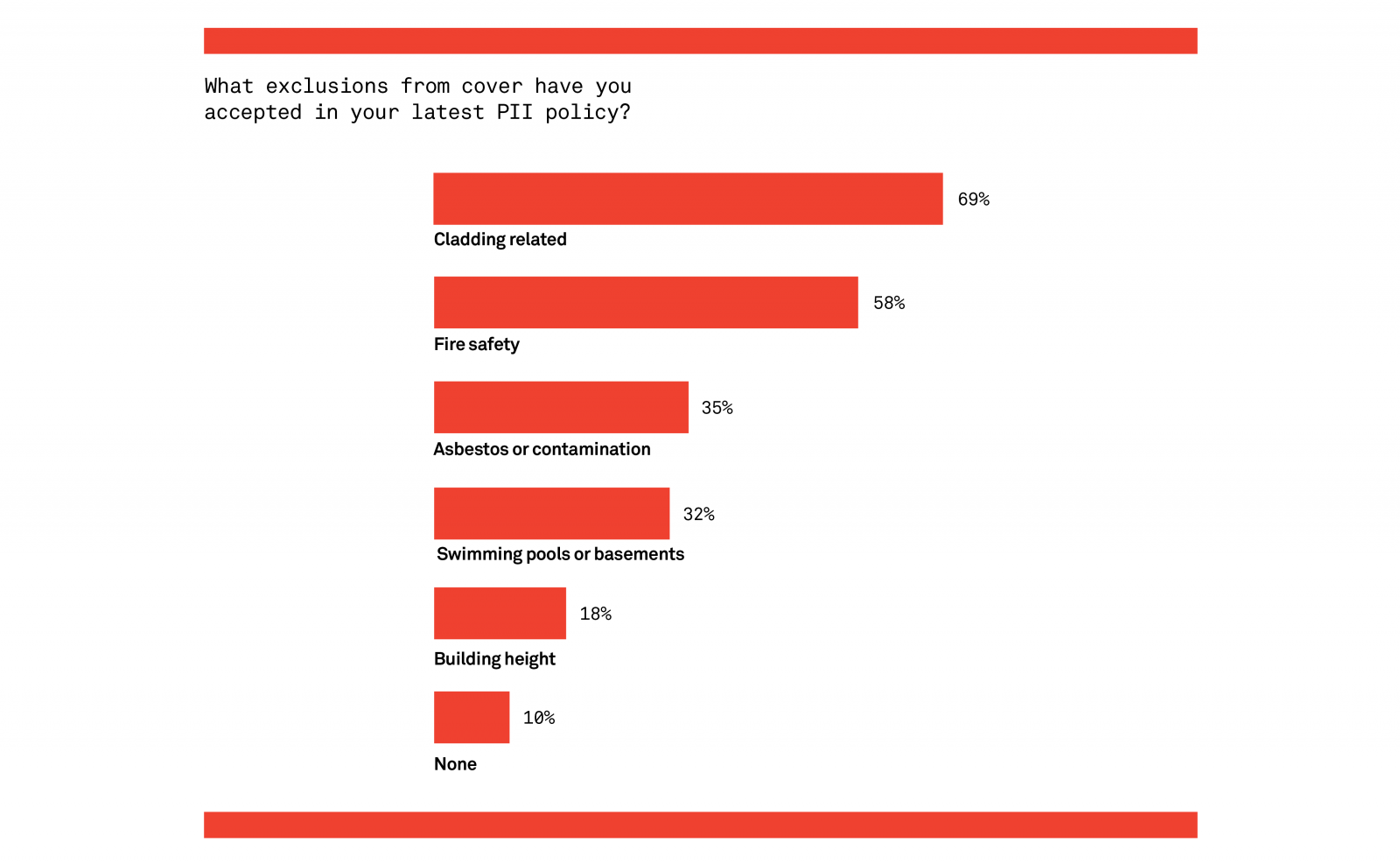

Like many architects at this time of year we have just renewed our Professional Indemnity Insurance (PII). The cost of premiums has rocketed in the last two years, in some cases tenfold. The principal reason for this is that the insurance market has adjusted the risk profile of architects post Grenfell. If lucky enough to obtain an insurance quote, architects now must court the market with extensive documentation that describes the business along with a catalogue of historical projects. Ironically there isn’t a “no claims bonus” reward here, even practices that have clean sheets and no cladding risk are seeing premiums rise exponentially. There is worse to come. Each year the list expands, fire, cladding, insulation, basements, are already included but watch out for current innovations like CLT and blue roofs to be added for example.

In many ways architects have only got themselves to blame. Our education system does not generate skilled technically proficient graduates. In a rapidly changing and increasingly complex industry, we are far too willing to rely on the designs of sub-contractors and perhaps worst of all, we have allowed Quantity Surveyors to drive “value engineering”. Usually exercised at the behest of clients this often leads to the delivery of a compromised and sub-standard product. I prefer to call this process “devalue engineering” as it rarely improves the value of the building in design or in quality. These cost driven decisions have design and sometimes safety consequences, as Grenfell demonstrated, but this is not reflected in a spread of risk amongst the design team, the cost consultants and regulators, compared to the burden that is loaded on the architects’ shoulders.

Novation is another area where architects are far too willing to acquiesce, it is often a requirement embodied in the architect’s appointment. Acting as a novated architect can often feel like being just another sub-contractor, bullied by an army of Main Contractor surveyors looking for further savings, and then battling to get your fees paid.

All in all, we have got ourselves into a sorry state, and where is our professional body in all of this? The RIBA seems toothless, this is the biggest issue facing architects today and it feels as if we are not being supported by our own Institute which seems to lack the will to represent the commercial interest of its members.

There is a fundamental issue here, architects will not get work without PII, clients insist on £5m, £10m, and sometimes £20m of cover, and therein lies the problem. PII has become part of our commercial offer to win work, not only do we cut fees, but we also offer to insure the risk as well. If PII is of value to the client then why don’t they pay for it?

Given the scale of investment, it is quite right to demand a level of competence from the design team, but if it is seen as a project insurance policy there is something fundamentally flawed in the process. Perhaps the answer lies in looking at the problem differently, if clients selected a competent team, and set up a bespoke and project-based insurance policy, the liability would be spread across the contractors and sub-contractors, fire engineers, designers, cost consultants etc. in a more proportionate manner.

Alternatively, I have often thought that if every architect stopped buying insurance across the board, the development and construction industry would perhaps look at how projects can be procured and built without assuming that they can rely on the safety net of the designers PII.

Finally, it is worth considering that over the last two years our practice's PII premium increase would employ 5-6 qualified and experienced architects. A much better way to de-risk a project surely?

With thanks to the Architect's Journal 'Insurance crisis: a ticking time bomb for architects' for the graphics.